July’s 6.5% Rent Spike: The New Landlord Gamble

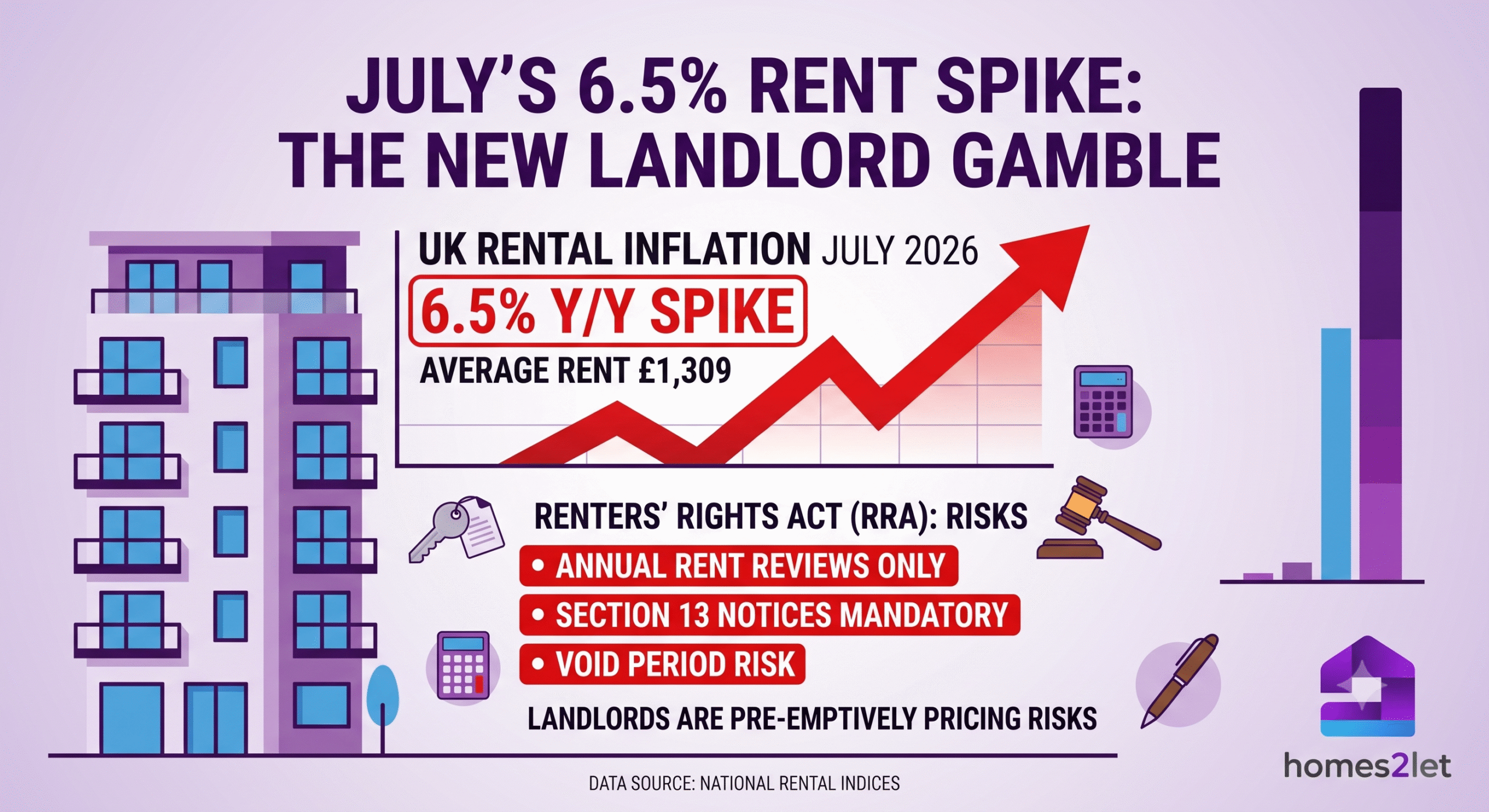

Under the new RRA framework, traditional rent review clauses are history. Landlords are now legally restricted to just one review a year, meaning they only get one shot every 52 weeks to adjust for inflation and rising costs. The result? Landlords are aggressively “front-loading” their asking rents right at the start of new tenancies. But in a cooling economy, asking tenants to swallow a 6.5% premium is a huge roll of the dice. Do it wrong, and a single vacant month will instantly wipe out your profits.

Anyone hoping the private rented sector would find a calm, predictable baseline after the Renters’ Rights Act (RRA) rolled out on 1st May is in for a rude awakening.

Fresh data from national rental indices out this week shows rental inflation across England has suddenly spiked by 6.5% year-on-year. That drags the average monthly rent up to £1,309—a near two-year high. If you look at the quieter, more stable market trends we saw at the start of 2026, this is a massive u-turn.

But don’t make the mistake of assuming this is just standard supply and demand at play. What we’re actually seeing is the first major, unintended side effect of the RRA: landlords are being forced to take a high-stakes gamble with their pricing strategy.

The Section 13 Trap: Why Asking Rents Are Being ‘Front-Loaded’

To understand why rents took such a sudden leap this July, you have to look at the massive shift in how landlords are now legally allowed to increase their prices.

Under the new RRA framework, traditional rent review clauses inside tenancy contracts are officially history. Instead, you’re legally restricted to just one rent review every 52 weeks. To do it, you have to serve a formal, statutory Section 13 notice, giving your tenants a minimum of two months’ warning. On top of that, tenants now have much stronger powers to challenge these increases at a First-tier Tribunal if they can argue the new price outpaces the local market rate.

Think about the position that puts a property owner in. When you know you only get one shot a year to adjust for inflation, rising mortgage rates, and skyrocketing maintenance costs, panic sets in. The result? Landlords are aggressively “front-loading” their asking rents right at the start of a new tenancy. They are pricing in future financial risks on day one because their hands will be tied for the next year.

The real risk: Sticking an artificially inflated price tag on your property to “future-proof” your cash flow is a massive roll of the dice. Do it wrong, and you’ll scare off great tenants, trigger a stressful tribunal challenge, or leave the property completely empty.

With wider economic wage growth sitting around 3.4%, asking tenants to swallow a 6.5% premium is a huge ask. Let’s do the math: a single “void month”—where your property sits vacant because you priced it out of the market—wipes out roughly 8.3% of your annual rental income. That instantly obliterates any extra profit you hoped to make from a higher monthly sticker price.

Turning an Investment Into a Full-Time Job

Let’s be honest: the private rented sector doesn’t look anything like it did a few years ago. Between the total abolition of fixed-term contracts—meaning every single tenancy is now a rolling, periodic agreement from day one—and the definitive end of Section 21 “no-fault” evictions, managing a buy-to-let portfolio has turned into a high-stakes legal obstacle course.

Trying to navigate rigid annual rent-review windows while chasing top-of-market prices to stay afloat isn’t a passive investment anymore. It’s a stressful, full-time job. But you don’t actually have to play by those rules.

Want to understand more? Watch this:

The Hassle-Free Alternative: Opting Out of the Open Market

Instead of stressing over statutory notice windows and gambling on whether a tenant can actually afford your inflated market rate, an increasing number of property owners are stepping off the traditional open-market carousel altogether.

By partnering with a specialist provider like Homes2let through a Guaranteed Rent Scheme, you can entirely insulate your portfolio from the friction of the Renters’ Rights Act. Here is how it changes the game:

- Guaranteed Cash Flow, Zero Voids: You get paid every single month, on time, in advance. It doesn’t matter if the property sits empty for a few weeks between occupants—your income remains identical.

- 0% Commission: Traditional letting agents love to eat into your yields with hidden management fees, renewal charges, and percentages. A guaranteed rent scheme keeps things transparent with absolutely zero commission.

- Total Legal Protection: The provider steps in to manage the periodic tenancies and deal directly with the occupants. You are completely shielded from court backlogs, eviction delays, and compliance headaches.

- Maintenance Handled: Internal, hands-on maintenance teams take care of the daily wear and tear. Your asset stays up to date with tightening property standards without you needing to pick up a phone at 2:00 AM.

The RRA hasn’t killed buy-to-let investing; it has just broken the traditional way of doing it. Rather than overpricing your property and hoping for the best in a volatile market, securing a fixed, guaranteed income gives you back the one thing the new laws tried to take away: total certainty.

Riz is the founder of homes2let and has been in real estate for over twenty years. He has a background in economics and is a real estate developer and buy to let investor.

You can get in touch with Riz via riz@homes-2let.com.

Related Insights

Landlords Face Tough Choices as EPC Deadline Looms

A new survey reveals that most landlords are aware of upcoming Energy Performance Certificate (EPC) regulations, but many are unprepared. Over two-thirds of landlords own properties that don't meet the new 'C' target, raising questions about how they will adapt. Will they invest in upgrades, pass the costs on to tenants, or simply sell up? Read on to discover the challenges and opportunities facing landlords in the face of these new rules...

The Shift in the UK Buy-to-Let Market: Navigating Landlords’ Sales Surge and Rising Rents

The UK real estate landscape is witnessing a significant transformation, particularly evident in the buy-to-let sector. The recent trend of landlords divesting their properties is reshaping the rental market across Great Britain, with a notable impact in Scotland. This article delves into the multifaceted reasons behind this shift, the consequent effects on the housing market, and the future outlook for investors and tenants alike.

What Landlords Need to Know About Current Eviction Rules

The national ban on residential evictions that ran for six months until 20th September, followed by the introduction of new six month notice periods for evictions which will be in place until at least the end of March 2021, have put additional pressure on landlords already facing tough times during the pandemic. So what can landlords do to find their way through these challenging times?